THE BALTIMORE BANNER

The housing hustle igniting a foreclosure crisis in Baltimore

Hallie Miller, Giacomo Bologna and Sahana Jayaraman

10/2/2025, Updated 10/10/2025

Excerpts, followed by comments on this article

(Alex Fine for The Banner)

(Alex Fine for The Banner)

The foreclosures could send neighborhoods spiraling and make Baltimore the center of America’s next big housing crisis

Diana Scott’s East Baltimore rowhouse isn’t perfect, but for the last five years, it’s given her family stability in an economy where everything from gas to groceries costs more.

Every month the family of five pays $1,100 — an attractive rent considering the value of the home has tripled during their tenancy, at least on paper. Then the foreclosure notice arrived.

Something peculiar is happening to Scott’s home, along with nearly a dozen more on her street and up to 704 across Baltimore. In concentrated pockets of the city’s East and West sides, many of the homes have hit the auction block this year at noticeably inflated prices. And no one is biting.

Scott’s home is part of a portfolio linked to New York buyers who leaned on a newly popular mortgage loan product to buy hundreds of homes in Baltimore. Private equity funds have fueled its rise, and with many of the mortgages now in default, lenders and noteholders have been left holding the bag.

Starting in June, at least five Wall Street-backed financiers blacklisted the buyers, as well as some of their associates and affiliated entities — and clamped down on lending in Baltimore.

But by then the New York buyers had amassed some $100 million worth of loans from at least two dozen private lenders, including AmeriTrust Mortgage Corp. and RCN Capital, according to public land records. At least half of the Baltimore properties in the New Yorkers’ portfolio are in or nearing foreclosure.

So many defaults could send neighborhoods spiraling and untether families like Scott’s. And it has the potential to make Baltimore a ground zero for America’s next great foreclosure crisis, dooming the effort to clear the city’s stock of vacant homes and scaring off investment at a time it’s sorely needed.

Over a four-month investigation, The Banner reviewed thousands of public property records, business filings, court records and private loan documents and analyzed real estate transactions and mortgage datasets. The paper trail leads to a New York buyer named Benjamin Eidlisz, who, for the better part of a decade, set his sights on making money in Baltimore.

Eidlisz jumped into Baltimore real estate in 2017, with a plan hatched out of an 800-square-foot office in an Orthodox Jewish community within Spring Valley, New York. Then he and a business partner, Benjamin “Bruce” Sherr, formed a limited-liability company called B&H Ventures and bought roughly 100 homes in Baltimore. Initially the profit margins were thin, but Eidlisz and Sherr planned to rent all the homes, refinance at a lower rate and turn a profit by year three, court records show.

On April 19, 2022, an entity called EGBE Ventures was organized in Maryland, using Eidlisz’s home address. It was registered in the name of Eluzer Gold, a Spring Valley, New York, resident who had a good credit score, according to personal financial documents reviewed by The Banner.

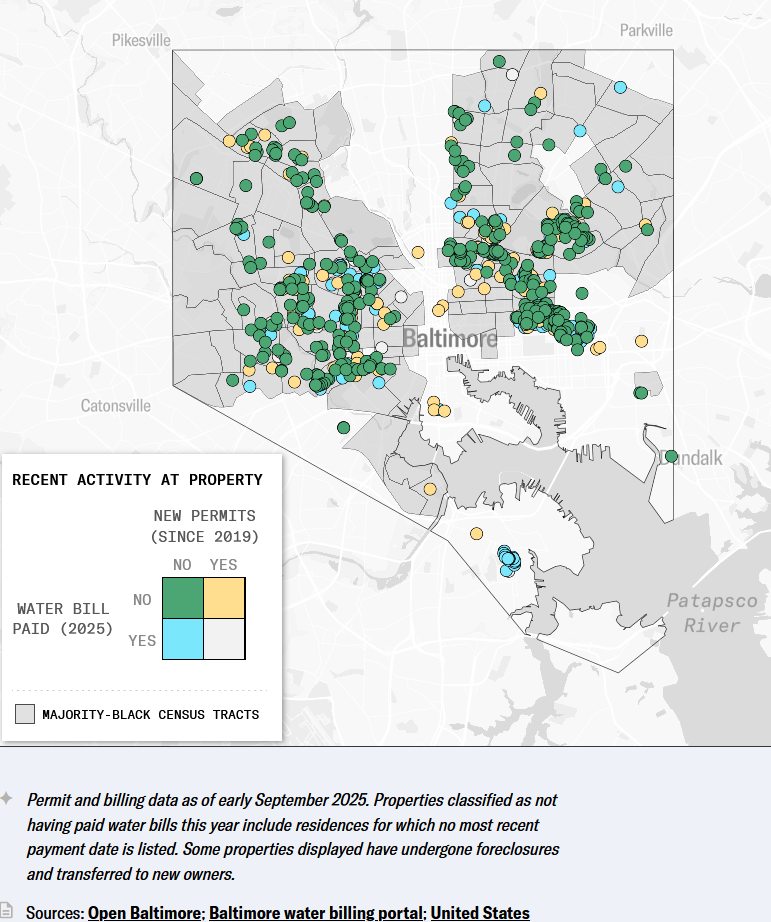

Despite pricey sales, the New Yorkers’ properties show few signs of improvement

Less than a third of the portfolio has received a construction permit since at least 2019, and less than a quarter has paid a water bill this year. Most of the properties are clustered in the wings of the “Black Butterfly” — a term coined by Morgan State University researcher Lawrence T. Brown to describe the majority-Black regions that fan out on either side of the city, where residents have historically been denied access to capital.

Permit and billing data as of early September 2025. Properties classified as not having paid water bills this year include residences for which no most recent payment date is listed. Some properties displayed have undergone foreclosures and transferred to new owners. Sources: Open Baltimore; Baltimore water billing portal; United States Census Bureau (2023 American Community Survey; one-year estimates)

A financial advisory group conducting a study for the Greater Baltimore Committee found an unexpected source of money flowing into the city. The researchers reported that financing with high interest rates and looser restrictions, or “hard money,” was helping to pay for investments in neighborhoods where bank money had historically been slow to flow.

It’s called a debt service coverage ratio loan, or DSCR loan. Landlords in Baltimore have been increasingly flocking to it in the past five years, a Banner analysis of national mortgage data shows.

With conventional mortgage loans — which are based on borrowers’ income — applicants are inherently limited on the amount they can borrow. DSCR loans are particularly attractive to landlords because they have less stringent requirements. To get one, an applicant needs a good credit score and to show that a tenant’s projected rent payment is greater than the homeowner’s monthly mortgage payment.

With these loans, a landlord doesn’t need to show proof of income or even that there’s a tenant lined up. And there’s no limit on how many they can get. With a DSCR loan, the lender needs the renter to pay the landlord, and the landlord must pay the loan. DSCR loans are generally considered higher risk, which is why most are issued by private lenders, rather than traditional banks.

DSCR lending activity spiked in Baltimore starting in 2021, a Banner analysis shows. Many lenders liked the deals because they could sell off the debt to private equity firms and insurance companies, including arms of industry giants such as JPMorgan Chase and U.S. Bank. The loans are bundled together in massive pools of mortgages and sold to investors worldwide as securities.

One of the nation’s major DSCR lenders is Dominion Financial, a private mortgage lender headquartered in downtown Baltimore that finances deals around the country. Jack BeVier, a partner at Dominion, said he’s seen firsthand how transformational these loans can be for communities overlooked by traditional banks.

Foreclosures rain down

But not long after, BeVier began noticing that Baltimore was seeing a wave of foreclosures on DSCR-financed properties. All the foreclosures were linked to the New York buyers.

Eluzer Gold owns several houses on Etting Street that have since defaulted. (Jerry Jackson/The Banner)

The New York buyers’ troubles highlight the need for increased regulation in lending, especially among private financial institutions, said George “Mac” McCarthy, president and CEO of the Lincoln Institute of Land Policy in Cambridge, Massachusetts. The situation closely resembles that of the Great Recession, McCarthy said. Lenders at that time were making thousands of ill-advised loans to keep the money flowing — in spite of the risks attached. Mass foreclosures caused by the DSCR loan failures could hit Baltimore hard, McCarthy said, tanking property values across the city. It will make Baltimore’s supply of vacant houses even more pronounced and harder to fix.

Many of the homes are even boarded up and abandoned, and others never reported a single tenant living there, bankruptcy records show. Of the hundreds of homes The Banner identified as connected to the New York portfolio, more than 70% haven’t had a single renovation or construction permit pulled since at least 2019, according to a Banner analysis of the city’s permitting data.

When private mortgage companies and their financiers caught wind of the foreclosures and Gold’s bankruptcies this past spring, DSCR activity ground to a halt in Baltimore. Foreclosures are raining down in East and West Baltimore.

While others are paying the price, the New York buyers haven’t stopped trying to make money in Baltimore. In July, Eidlisz reached out to a lender to try to buy, sell and refinance a bundle of homes, according to an email exchange reviewed by The Banner. This summer, judges allowed one of Eidlisz’s companies to take over the management of more than 200 of Gold’s properties in bankruptcy.

The bankruptcy documents don’t mention Eidlisz’s transactions with Gold, aside from saying that Eidlisz once served as Gold’s property manager. Under the court-approved agreement, Eidlisz’s company will earn $227,000 in one-time fees, plus $24,000 a month, to manage the properties.

_______________________________________

Comments

The following comments are extracted from a Common Ground USA member forum, the first from Scott Baker, Oct 28, 2025:

They aren’t just buying houses. They are dismantling the American Dream, piece by piece, with a playbook so sinister it would make a Bond villain blush. A few weeks ago, BlackRock allegedly bought 50,000 homes. Then, they sold three to themselves for more than double the price. Your neighbor’s home value just “doubled” overnight. Congratulations. Now you can’t afford the property taxes to live there anymore. This isn’t an accident. It’s a calculated corporate heist. Here is their step-by-step playbook:

STEP 1: THE HUNT They use algorithms and vast data to identify stable, middle-class neighborhoods with untapped “growth potential.”

STEP 2: THE BLITZKRIEG They show up with unlimited corporate cash. They don’t need mortgages. They offer 20%, 30%, even 50% above asking price. Imagine you list your home; a young family makes an offer. Then a corporate entity swoops in and says, “We’ll pay $100k more, in cash.” The family never stood a chance. The community is gutted before the “For Sale” signs even come down.

STEP 3: THE SQUEEZE Regular families are now permanently priced out. How do you compete with a bottomless wallet? You don’t. The dream of homeownership is extinguished on your own street.

STEP 4: THE ILLUSION Once they control a critical mass of homes, the real magic happens. They sell a handful of properties to shell companies they already own. It’s a game of three-card monte, but with the roof over your head.

STEP 5: THE NEW “REALITY” Those fake, inflated sales to themselves are now logged in public records. Suddenly, a $300,000 home is “worth” $700,000. This becomes the new, fraudulent “market rate.”

STEP 6: THE FINAL NAIL – THE TAX TRAP This is where they force you out. Property taxes [throughout your neighborhood] are reassessed and TRIPLE based on those fake sales. The elderly couple on a fixed income, who paid off their home 20 years ago, can’t afford $15,000 a year in taxes. The young family that scraped together a down payment is now house poor.

THE ULTIMATE INSULT: YOU WILL OWN NOTHING, AND YOU WILL BE HAPPY TO RENT FROM THEM. They created the problem. They priced you out. And now, they become your landlord. The mortgage payment would have been $1,800. Your new rent [payment] to them is $2,500. You are now a permanent tenant in your own neighborhood, funding the very machine that evicted you. This isn’t capitalism. It’s a hostile takeover of the foundational pillar of American life. It’s financial warfare against the middle class.

More evidence:

This is disturbing because Blackrock (actually, it’s Blackstone) has been accused of snapping up vast amounts of real estate nationwide.

https://en.wikipedia.org/wiki/BlackRock_house-buying_conspiracy_theory

From Marty Rowland to Ed, Scott:

Excellent post. I saw this one last week. It fits well within the course I’m teaching on rentier capitalism. This sleight of hand would not be possible if the full increment of land value were captured, but it wasn’t, so there’s nothing in the story that says anything about the utility of LVT [Land Value Taxation].

This is a story of a land rentier who has the privilege of being a master landlord who then uses that advantage to exercise financial rentierism by jacking up the price of a commodity with the “rules of the real estate game”. Henry George would say the solution is capturing the land value completely (incrementally), and by doing so the newly minted $700,000 homes would never sell and the scheme would collapse because the jack up price increase is pure economic rent. Blackstone would not be able to collect enough rent to pay the increased land value tax.

_____________________________________________

Additional comment from Tom Gihring, Common Ground – OR/WA

Historically, private interests and complicit politicians have used housing policies to hoard wealth, pushing indigenous communities from their lands and enacting policies that prohibited people of color from homeownership. Today, real estate speculators and corporate landlords are scooping up properties in Baltimore and cities around the country, pricing would-be homebuyers out of the market and pushing tenants out of their homes with rent hikes.

What is needed is a tenant empowerment tool that seeks to address the power imbalance between property owners and their renters who have to absorb excessive mortgage payments. An opportunity to purchase law would advance the transfer of property ownership into the hands of tenants and affordable housing developers by enabling tenants to exercise a first right of purchase when the landlord chooses to sell. Landlords would be required to give notice to tenants and then allow a period of time for tenants to express interest, make an offer, and secure funding. If tenants don’t choose to own, they can assign or sell their rights to a non-profit housing corporation such as a community land trust, or other reputable owner of choice. Such a law (named TOPA) has seen success in Minneapolis.

This scheme works in conjunction with the land value tax. Remember, with LVT the taxing authority captures the land rent which will be substantial because the land-to-building value ratio is high. The elevated tax burden raises the holding costs of the property, reducing the landlord’s profit margin. It also has the effect of capitalizing the value of the over-priced property into a lower selling price. This in turn benefits the designated buyers who now have a more affordable dwelling.