![]()

Common Ground OR-WA

ORIGINAL RESEARCH

How a Land Value Tax Can Stimulate Investment in Housing

By Tom Gihring

February 2018

Recent studies by Portland’s City Club and the League of Oregon Cities have shown that Oregon’s property tax system, due to the cumulative effects of Measures 5 and 50, is broken. Since 1993 Oregon has been saddled by the ill-conceived M-50 tax limitation that caps annual growth in assessments to three percent. Over the years the ‘taxable’ assessments have lagged far behind true market values, especially in rapidly gentrifying neighborhoods like Alberta Arts District and more recently Eliot.

Considering the current housing crisis, it’s time to look at ways state property tax reforms can contribute to a solution to the gross inequities present in the current tax system. We believe the best fix is a return to true market assessments and land value taxation, a shift of tax rates off buildings onto land values.

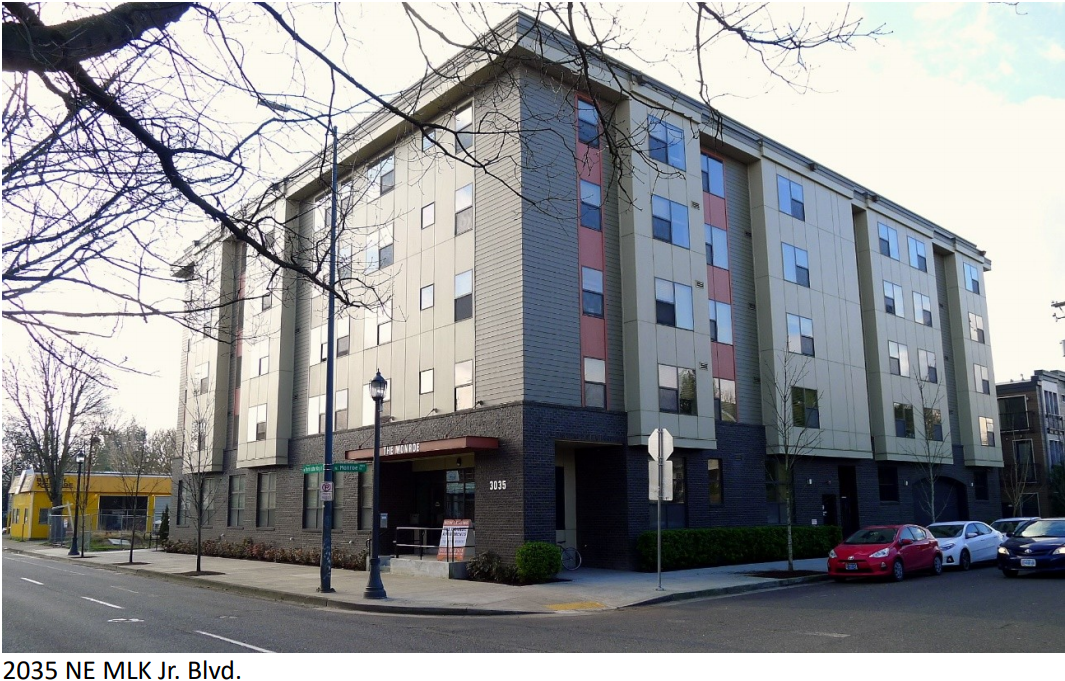

The NE Martin Luther King Blvd. corridor within the Eliot neighborhood is experiencing an influx of new development; the intersection at NE Morris St. is an example. Following a disastrous fire in 2013, construction was completed on the Monroe apartments at 3035 NE MLK in 2016. Other developments quickly followed, including an adjacent residential building on NE Morris St., and the 1.5-acre Garlington Center across the street on NE MLK integrating 52 affordable housing units and health care services. Still remaining is a lonely corner lot at 3007 NE MLK now available for redevelopment.

How do property taxes play a role in owners’ decisions to either hold onto vacant and underutilized land or invest in building improvements? With a bit of modeling, we can estimate the incentive effect of a land value tax (LVT) on two sites cited here. First, LVT always uses true market value (TMV), never the maximum assessed values(MAV), or “false” values that conform to Measure-50 limits. Therefore, the specific property tax proposal illustrated in this example would make two changes from Oregon’s current system: 1) applying the property tax to RMV assessments instead of the conventional tax method that uses MAV assessments, and 2) taxing land at a higher rate than improvements. How much? That’s a matter of judgement. We will simulate a LVT application that increases the tax rate on land to 80 percent of the total rate. The assumption is that Multnomah County will adopt a local-option LVT, whereby a revenue-neutral differential tax rate will result in the same total county-wide revenue under both the conventional and LVT systems.

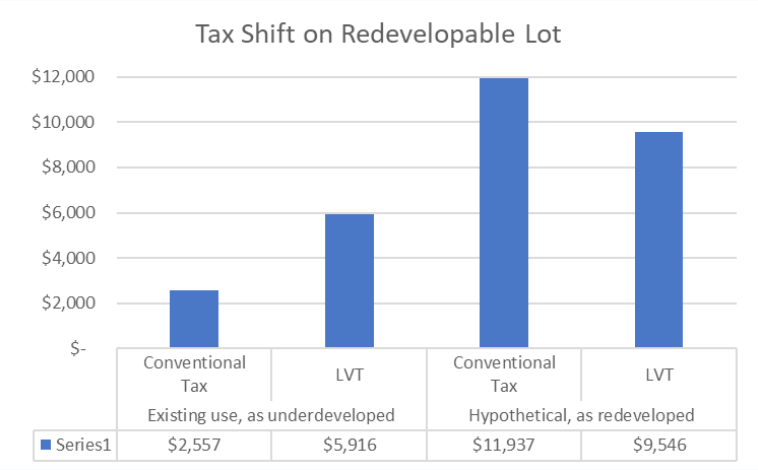

1. First, let’s examine the underutilized lot on NE MLK Blvd., comparing the property in its current state and its redeveloped state (as a hypothetical); tax outcomes under both tax systems will be compared. Using current county assessments, the MAV of $102,290 is less the TMV of $467,200. In fact, the TMV is 4.6 times as much as the MAV, revealing how far from reality the M-50 assessments have drifted. The conventional mill rate of $25 per thousand assessed value for Levy Code Area 710 yields a tax of $2,557.

The MAVs for the whole of Multnomah County are about half the TMVs. If we change the tax base to TMV, the effective rate is $12.87. Next, we split this total rate so that the tax rate on the TMV land assessment is 80 percent of the total rate; that gives us a land rate of $23.94 and a smaller $5.98 rate applied to improvement assessments. This split rate applied to the subject lot’s land and building TMV assessments yields a current annual tax of $5,916. That’s a positive tax shift of 131 percent.

Why is LVT often termed “incentive taxation”? Consider this – If the existing or a new lot owner reckoned the higher tax burden added too much to the land carrying costs and decided to demolish the small workshop now for sale and construct a $900,000 apartment building on this site, the tax outcomes from the conventional tax and LVT regimes would stand out in sharp contrast. First, the adverse and convoluted effects of the current system: Oregon law accompanying Measure 50 requires county assessors to adjust the MAV when major changes are made to a property. Changes such as new construction are “exceptions” that trigger the increase of the property’s MAV to an amount closer to TMV. You can see where this is going… If land owners invest their own capital in building improvements the reward is a jump in the assessment and higher taxes; whereas if they hold onto underutilized sites waiting for the land value to rise and capturing the ‘windfall’ at sale they are rewarded with low taxes.

Under the exceptions rule, MAV is recalculated by applying a factor called the property change ratio (PCR) to the TMV – this gives an adjusted MAV of $477,485. Now the conventional tax yield at the $25 mill rate is $11,937. The total RMV of this hypothetically redeveloped site is $1,073,820. Using the split rate of the land value tax (23.94 / 5.98) and applying it to RMV land & improvement assessments, the tax outcome is now $9,546. That is a 20 percent reduction in tax burden due to the low ratio of land to improvement value – the investor’s fairer reward.

2. Secondly, let us examine the before & after comparative tax incidents on the Monroe apartments at 3035 NE MLK, using the property in its two states: it’s undeveloped status in 2012, and it’s completed development in 2016. We shall try and abbreviate the narrative on this scenario.

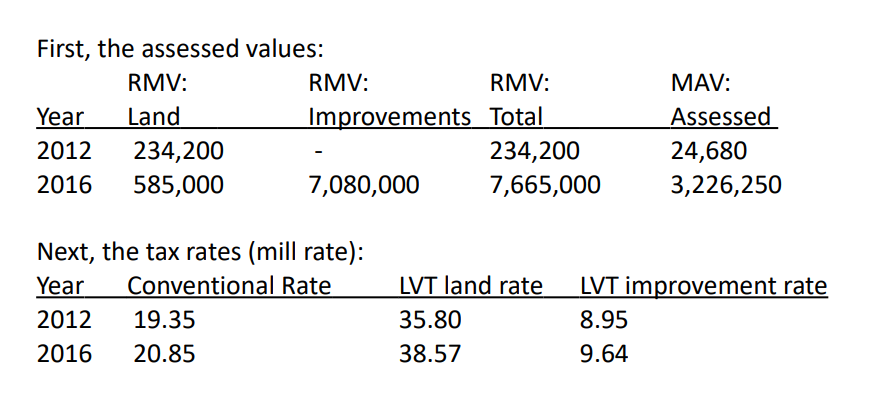

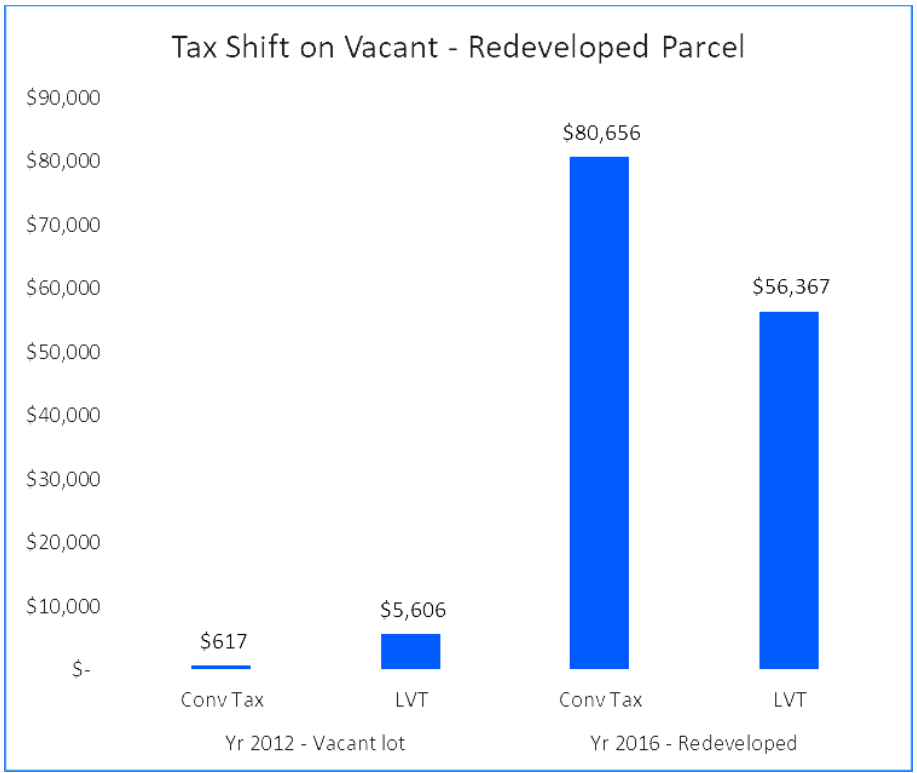

As an unimproved lot in 2012, the real market value was 9.5 times the MAV which is used to determine the tax. Again, we see how distorted the effects of M-50 limitations have become. The 2012 tax bill calculated in this model is a mere $617. If a land value tax had been in effect, the same year’s tax bill would have been $5,606, that is 9 times higher than the conventional tax. Such a shift in tax burden might have motivated the decision to more quickly develop the site or sell it to a developer. As a developed parcel in 2016, the reward for putting this land into more productive use becomes evident. The conventional tax on the $3.2 million MAV is $80,656. By comparison, the land value tax yields $56,367; that is 30 percent less. The reduction, of course, is attributed to the high ratio of building-to-land value on this site and the low tax rate on improvement assessments.

The findings in this modeling exercise are borne out by the state of Pennsylvania’ experience with a land weighted property tax. Currently, 19 cities in Pennsylvania use this form of incentive taxation. Consider Harrisburg: in the late Seventies, it was one of the least desirable cities in the country in which to invest, with some 2,000 boarded up businesses. After phasing in its current tax structure to capture the publicly created value in land, Rand Corporation named it a Most Livable City in 1987 and 1988. Housing is more affordable than in similar cities with worse economies because a higher tax on land values helps dampen residential price inflation. It’s simple: tax residential buildings less and the supply expands. We do not suggest that the LVT will change every land owner’s investment decision through a tax shift. But, the effects in the aggregate are significant.

PDF: MLK parcels – LVT Incentive effects